2 Ways to Prepare For the Commodity BullRun

2 Ways to Prepare For the Commodity BullRun

The demand for two commodities is growing exponentially, but do you have exposure to them?

This week, we’re going to take a look at Livent Corporation (NYSE: LTHM) and Energy Fuels Inc. (NYSE: UUUU), which are plays on the rise of lithium and uranium, respectively.

I see these as two essential commodities of the future. Lithium will benefit from the future of energy storage, and uranium production will return to relevance in the U.S. as nuclear energy becomes more prominent.

Their stocks are also somewhat uncorrelated with growth stocks — as we’ve seen in recent weeks — which gives our Disruptors Index some balance.

We’ll also take a look at the CPI and retail sales data that came out last week, and what we can expect as a reaction from the Fed.

For a condensed update, watch the video below!

Uranium

Nuclear energy is rapidly gaining attention across the globe. One of the biggest reasons for this shift is the energy crisis unfolding right now, primarily in Europe.

France’s Électricité de France, one of the largest nuclear power generators in the world, plans on having all 56 of its nuclear reactors up and running this winter. This includes three of the most powerful nuclear facilities in the world.

In Germany, nuclear power accounted for over 12% of all electricity generation in 2021, but that’s fallen to just 6% this year. However, due to rapid increases in oil and gas costs, they’re already looking to restart the reactors they closed earlier this year.

Japan’s nuclear production is down nearly 30% since the Fukushima meltdown of 2011. However, they’re also looking to reverse that trend starting as soon as next year.

At the heart of nuclear energy, of course, is uranium. And with countries all over the world looking to make nuclear a bigger part of their electricity generation, we’re looking at much higher demand for this metal.

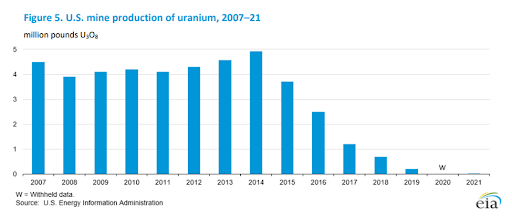

In the U.S., production of uranium was reduced to essentially zero over the past seven to eight years, as you can see in this chart:

Source: U.S. Energy Information Administration

In 2021, only 21,000 pounds of uranium was produced.

So far, 2022 hasn’t been much better. In the first half of the year, production was 15,988 pounds — on pace for a 52.3% rise from 2021, but still nowhere near the more than 4 million we saw in the early 2010s.

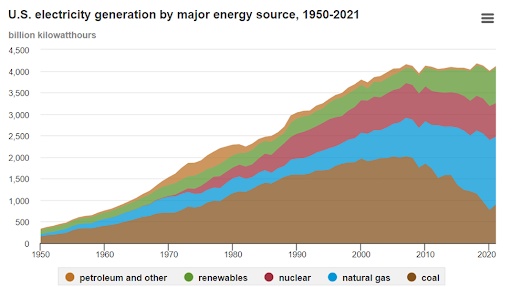

What’s even stranger is that the U.S. hasn’t really curbed its nuclear power generation during this time, as you can see in this chart:

Source: U.S. Energy Information Administration

We’re still using the same amount of uranium, but we’re now fully reliant on other nations to supply it. With growing geopolitical instability and the trend of deglobalization becoming more obvious, it would make much more sense for the U.S. to produce uranium domestically, as it did for past decades.

Energy Fuels Inc. (NYSE: UUUU)

Let’s start off with Energy Fuels Inc. (NYSE: UUUU), which is one of just three companies currently producing uranium in the U.S. They made the right move by continuing production here, and the benefits of this are already becoming obvious.

May was a huge month for Energy Fuels, as they entered into three new contracts with U.S. utilities to sell between 3 million and 4.2 million pounds of uranium from 2023 to 2030.

Not only does this mean that companies see the value of buying domestic uranium, but it also gives us a taste of the magnitude of demand that Energy Fuels is going to see in the coming years.

June was also a rewarding month, as the Department of Energy announced they expect to buy up to 1 million pounds of uranium from four domestic producers for its new Strategic Uranium Reserve.

With Energy Fuels being the largest producer in the U.S. sitting on over 600,000 pounds of uranium, it seems very likely that they’ll be a key supplier in this venture.

These deals are huge, not only in terms of size, but also importance. However, Energy Fuels is prepared for much more, as their White Mesa Mill alone is licensed to extract 8 million pounds of uranium per year.

Not only are they in a great position in the U.S. uranium production field, but their finances are also in order. As of the end of June, they have $98.2 million in cash, $43 million worth of uranium and vanadium (their second-largest production commodity), and zero debt.

It’s been a rough few years for Energy Fuels in terms of revenue, which is no surprise given the current state of the U.S. uranium market. But things are certainly looking up.

Over the past year, they’ve brought in $11.8 million in sales — an 81% drop from 2015, but a 594% increase from this time last year.

I believe that the worst is definitely behind them now, and in the coming few years, we’ll see them surpass what they made in 2015.

Lithium

Lithium is another essential part of the future of energy as it’s a key ingredient in the energy storage business.

As renewable forms of energy like solar, wind, and hydroelectric continue to become implemented on a larger scale, lithium-ion batteries will be used to store the energy for later.

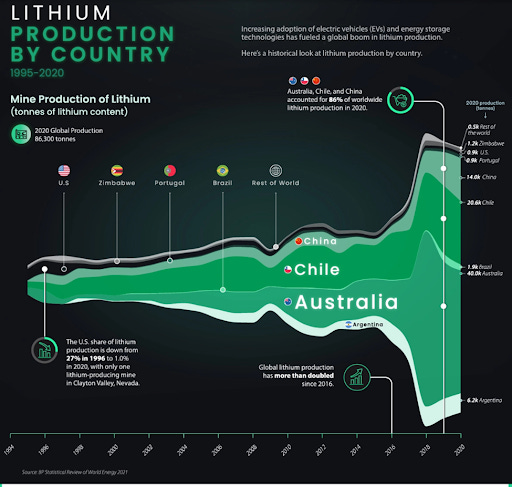

However, like uranium, the production of lithium is concentrated in very few places. As you can see in the chart below, 86% of lithium production in 2020 happened in just three countries: Australia, Chile, and China.

Source: VisualCapitalist

Another thing about this chart that may stand out to you is that the U.S. was once the largest producer of lithium in the world, accounting for 27% of global production.

Unfortunately, that’s no longer the case. Now, we only produce 1% of the world’s lithium. The sad truth is that we have just one operational lithium mine, which seems even crazier when you add in the fact that our lithium resources are the fourth-largest on the planet.

Nevertheless, the demand for lithium around the world is going to grow rapidly for years to come. In our portfolio, we’re betting on Livent Corporation (NYSE: LTHM) to emerge as a major player in this lucrative industry.

Livent Corporation (NYSE: LTHM)

As I pointed out, there’s currently only one functional lithium mine in the U.S., so unfortunately, there aren’t many ways to play the inevitable U.S. lithium boom for now. But until then, I believe Livent is one of the best bets out there.

Livent has become an increasingly relevant name in the lithium industry over the past few years, which has resulted in contracts with huge companies such as Tesla and General Motors.

Their most recent notable contract win happened less than two months ago, when they entered into a contract to supply GM with lithium hydroxide from 2025 to 2031. Within this deal, we can see Livent’s plans of transitioning their business into the U.S. as well.

Right now, the lithium hydroxide that they’ll sell to GM is being shipped up from Livent’s Argentina facility. But over the course of the deal, they aim to have it all processed domestically. This will certainly be a huge boost to Livent’s already strong sales growth.

In addition to the fact that their sales are up 68.8% in the past year, they’ve also seen their margins improve after being demolished by lockdowns and other restrictive COVID policies (along with virtually every other mining company on the planet).

In fact, their profit margin in the past year is 18.36%, which is the highest it’s been since 2018.

They’ve used a lot of their cash flow to recover and further scale their business after a rough 2020, but they’re currently sitting on $49 million in cash and an additional $156.3 million worth of inventory compared to $241.2 million worth of debt (of which just $13.5 million is due in the next year).

I don’t see demand for lithium going away, and I think it’s unquestionable that it’ll remain higher than supply. Livent should continue to grow their market share and, going forward, it’ll be exciting to see more partnerships come their way.

LTHM is one of many stocks positioned to soar when liquidity enters the market. But you want to be in on these stocks before they take off. For solid stock picks like LTHM, check out our Gold Membership.

Performance Update

21 Disruptors Index: -6.29%

S&P 500: -4.45%

Nasdaq: -5.22%

Russell 2000: -3.67%

ARKK: -4.73%

Top 3 Performers:

Enphase Energy Inc. (Nasdaq: ENPH): +3.44%

Tesla Inc. (NYSE: TSLA): + 3.13%

Livent Corporation (NYSE: LTHM): +0.61%

Bottom 3 Performers:

Ethereum (ETH): -20.82%

Energy Fuels Inc. (NYSE: UUUU): -12.76%

Desktop Metal Inc. (NYSE: DM): -12.29%

Energy stocks led the pack over the past week as Enphase Energy Inc. (Nasdaq: ENPH) and Livent continue to trade right around their all-time highs. Tesla Inc. (Nasdaq: TSLA) rounded out the Top 3 Performers — the only stocks in positive territory during a rough week across the market.

It was an unusually rough week for Ethereum (ETH) as the post-CPI selloff on Tuesday and the “sell the news” reaction to the merge on Thursday delivered two separate blows to the price.

That being said, I’m still very bullish on post-merge Ethereum, and price action like this in a crypto bear market is nothing out of the ordinary.

When the time comes for another crypto bull market, I still believe that ETH will rally 20X to 25X from wherever it bottoms out. If the bottom is in, which I’m still 50/50 on, that would put the top of the next bull market in the $17,600 to $22,000 range.

CPI

There’s no hiding it: The CPI data that came out last Tuesday was ugly. I don’t mean the fact that total CPI was actually down from July, but the trend in the underlying data isn’t exactly ideal.

The market clearly didn’t like the numbers either, with stocks selling off rapidly even before the opening bell.

To me, this is because of one major thing: core CPI, which measures inflation in everything other than food and energy.

While everyone was focused on energy prices going down once again, energy doesn’t affect core CPI, and lots of other things were actually up month-over-month.

For example, the “shelter” component — which measures real estate prices (though in a very strange way) and accounts for 32.4% of CPI — is still going strong, and retail goods actually made a comeback.

The “commodities” component — which measures a variety of retail goods and accounts for 21.7% of the total CPI — was up 0.53% from July, its second-largest increase in the past six months.

This is a huge and, therefore, very influential part of the CPI, slightly less than food (13.5%) and energy (8.8%) combined.

Overall, core CPI came in at 6.3% year-over-year. While that isn’t as high as total CPI, it’s the highest core CPI reading since March, which suggests that the inflation trend is still far from over.

Core CPI has been stubbornly sticking around, with consistently positive month-over-month readings for each month of 2022.

In August, it was up 0.6% month-over-month. Twelve months of that, and you have 7.4% inflation. Considering core CPI is 6.3%, that means the trend is once again heading the wrong way.

Why Did Core CPI Rebound?

The key difference between food and energy inflation and core inflation is what actually causes each one.

The reason food and energy prices go up is typically due to some issue with supply rather than demand. When supply is low, sellers have to raise prices in order to maintain the level of income necessary to run their business.

Of course, this can also easily lead to higher demand (especially with food) as everyone wants to stock up on whatever is in short supply.

With pretty much everything else, inflation is caused by too much demand. When energy prices are low, people theoretically have more money to spend, so they go out and buy more things.

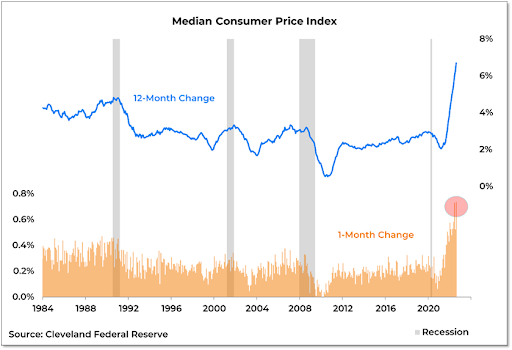

In this case, an extremely wide variety of line items in core CPI saw increases, and it pushed monthly median CPI up to a record high:

Source: @WillieDelwiche

Granted, this metric wasn’t tracked in the 1970s when inflation last saw more than 8%, but it still shows that inflation is affecting so many things that it’ll likely stick around for a while.

Where Is This Money Suddenly Coming From?

We know just about everyone has been feeling the effects of inflation over the past 12 to 18 months, so how are people now suddenly spending more? If you look at the amount of savings people have, it doesn’t seem to make sense.

Here, you can see that all the stimulus money has already been depleted, and total personal savings was sitting at $932 billion in July, the lowest amount since June 2016:

Source: TradingView

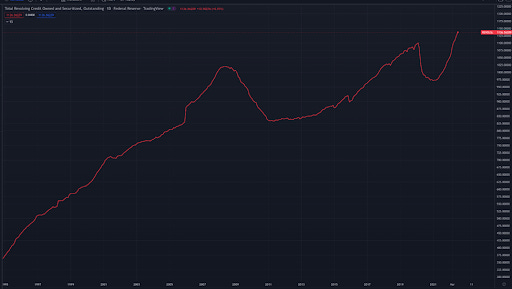

However, when we look at credit card debt, we get a totally different story.

Here, you can see that the weakening economic conditions haven’t really curbed credit card activity at all, as debt made its fourth straight all-time high in July at a massive $1.14 billion:

Source: TradingView

That might be the highest in 12 years, but it’s still a far cry from the mid-2000s, when people racked up four times as much revolving debt as they had in savings.

Still, this isn’t the trend we want to be seeing — especially when the Fed is keen on raising rates until the “consumer strength is solved.”

Implications

During July and August, the good economic data was celebrated because it meant that there may be a chance of a soft landing and/or a Fed pivot in the next few months.

The narrative of “low energy prices = good for inflation” also persisted. While that does have some truth to it, we would ideally want to see low energy prices, as well as low discretionary goods inflation.

I think this CPI data was a wake-up call because good economic data that suggests an increase in economic/consumer health (aka people are spending more money) means that there’s a good chance inflation will be higher.

More specifically, if this is the case when energy prices are down, it means that core inflation will be higher. That’s because core inflation measures the increase in price for discretionary goods that people hadn’t been buying due to the sky-high energy prices earlier in the year.

This type of inflation is dangerous in its own way, especially when the Fed’s stance is to crush inflation no matter what. They can’t really do anything against supply-based inflation, but they can certainly make an impact on demand.

The demand-based, or discretionary, spending is something that can be “solved,” to put it nicely. This is basically done by deliberately making economic conditions worse.

The Federal Reserve does two main things to achieve demand destruction:

1.) Raise interest rates, which increases the cost of debt, as well as its difficulty to pay back.

2.) Sell their assets like Treasury bonds back to the market, which dilutes the price of bonds, mortgage-backed securities, etc., and removes cash from circulation.

So, when they see any signs that the “consumer looks healthy,” the decision for them is clear: raise rates to reduce demand and essentially cause a recession.

Conclusion

My thought on this is that we won’t see this inflation trend really begin to subside while the labor market is strong. If people have jobs, they feel comfortable spending more.

They were still spending more back in the first half of the year — the difference is that now they don’t have to spend as much on energy, so they’re substituting it with other things.

At the same time, they’re continuing to add up more debt despite high interest rates and unimpressive levels of savings.

I think we’re still at least four to six months away from a material change in the job market and, until then, I expect inflation to stay relatively high and the Fed to keep raising rates — even if it’s at a slower pace.

Thanks for the update Ian.