Q1 Macro/Markets Update

What I'm Seeing In The Economy And How It Could Affect The Rest Of 2023

To cap off the quarter, I wanted to post a general update on what we’ve seen this year, and what I expect to see over the coming weeks and months.

Obviously, my strategy so far has leaned towards put buying, which generally hasn’t been successful as the market continues to find a bid.

The resilience in the market has been surprising to me, but my conviction that we’ll see lower prices and lower lows this year is still strong, and it stems from several trends that the market is currently defying.

1. Earnings recession

2. Weak business activity

3. Credit crunch

4. Finding safety in dangerous places

1. Earnings recession

I covered this at length in January, but lots of companies, especially in cyclical sectors, are seeing huge margin contraction. That means their expenses in 2022 went up more than their revenue, which leads to a smaller increase or even a decrease in profits. Later in this update, we’ll see exactly how this effected the largest companies in the market, but for now let’s take a look at the S&P 500 as a whole.

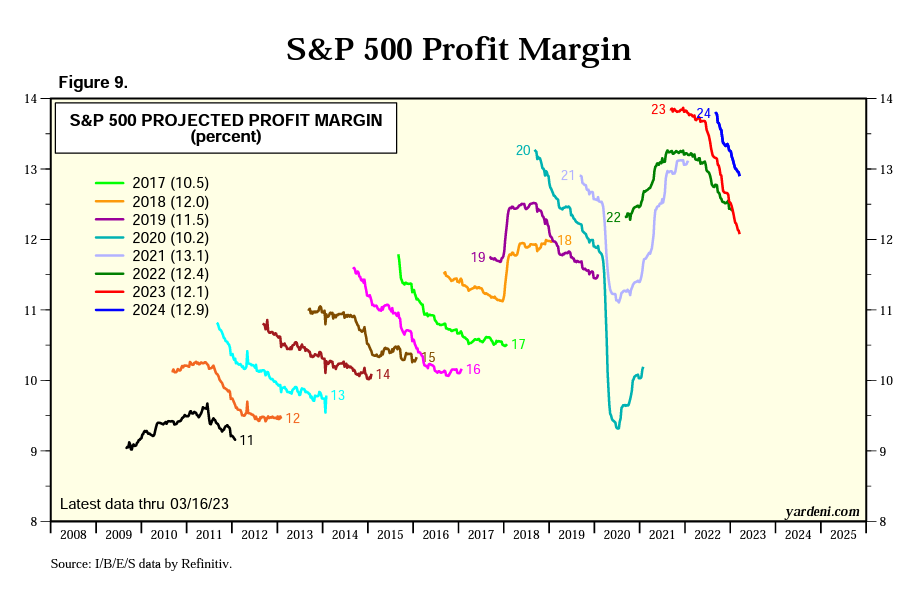

As you can see here, the profit margin expectation for the S&P 500 this year (the red line) has dropped off noticeably from just a few months ago:

A few months ago, the S&P 500 was expected to a profit margin of almost 14%, but that’s now dropped to 12.1%, which is lower than the 12.4% we saw in 2022 and the 13.1% from 2021.

Widespread falling margins are one of the telltale signs of recession, and are a direct cause of layoffs. When companies’ expenses outpace their sales, they feel pressure to cut costs, and the most common way to do that is via layoffs. We haven’t seen that trend develop yet, but I expect it to pick up speed in Q4 of this year.

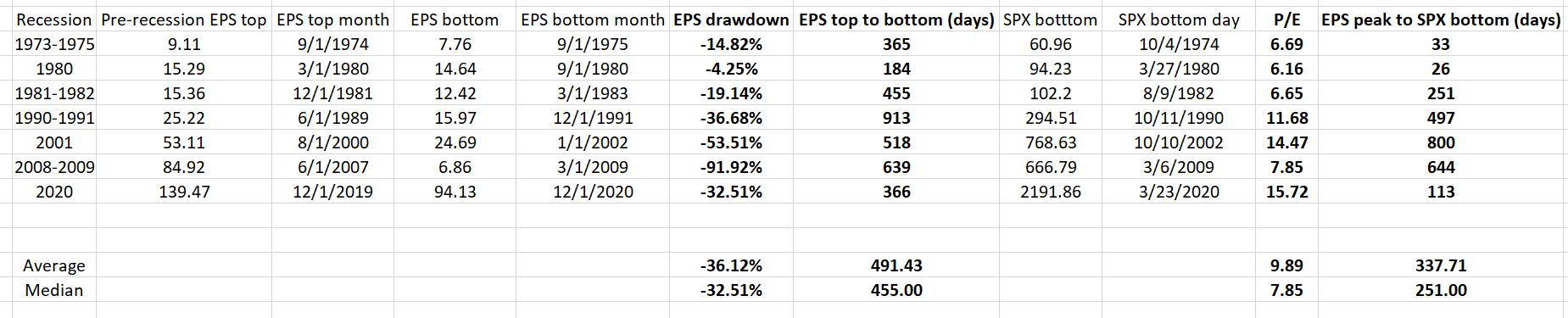

Assuming we’re heading into a recession, it’s also worth looking at how the earnings picture developed throughout past recessions. I went back through the recessions of the past 50 years and found some interesting trends. Here’s a chart with some data from each one, and then I’ll go over some key takeaways:

Now, here’s what I get from that:

1. EPS drawdown from the cycle top averaged about 36%.

2. Time between EPS top and bottom averaged 491 days

3. S&P bottom price divided by EPS top averaged 9.89

4. Time between EPS peak and S&P bottom averaged 338 days

(Side note: take all these estimates with a grain of salt; I’m just trying to provide some sort of framework for how we can expect this year to develop).

This cycle, annual EPS topped out at about $198 for the index in March 2022

If we go from 3/31/2022, that puts the EPS bottom in the high-120s, and it’d happen around July/August 2023.

The estimate for the bottom of the market would be 9.89 x 198, which is about $1,958 for the S&P 500. Even if we take the highest P/E (price to earnings) ratio from recent recessions of 15.72, it’d still put the S&P bottom at 15.72 * 198, or $3,112, which is still a decent amount lower than the $3,491 low to-date.

Finally, it would’ve put the S&P bottom price in Feb/March, which obviously didn’t happen. I’ll note that this cycle is definitely more drawn out than prior cycles due to the unprecedented level of stimulus, and as a result we’ve seen leading indicators flash major warning signals while things like the labor market and service industry activity continue to be very strong.

The point of going through all that is to explain how earnings matter to market prices. Right now, the market is defying the trend of lower margins and negative profit growth, but I do expect reality to hit at some point. The general expectation right now is that earnings will have a strong rebound in the second half of the year, but as you’ll see later in this article, that could easily go in the other direction as other parts of the economy, as well as credit activity, could hurt earnings over the rest of the year.

It will be interesting to see how the 2nd half rebound forecast evolves over the next 3-6 months, and I’ll be on the lookout for companies giving more clarity into what they’re seeing for the rest of 2023 during the upcoming earnings season.

2. Weak business activity in Manufacturing & Services sectors

Keep reading with a 7-day free trial

Subscribe to Ian Dyer to keep reading this post and get 7 days of free access to the full post archives.