Rate Hikes Claim Their First Major Victims

Rate Hikes Claim Their First Major Victims

Silvergate and Silicon Valley Bank are done. What happens next?

I was going to save the topic of debt for a future article, but it became very relevant earlier than I expected.

Right now, we’re seeing the first real signs of trouble caused directly by rate hikes. Just as 2022 was the year of the rate hikes, 2023 will be the year of consequences.

How SI and SIVB met their fate:

The two primary victims so far have been Signature Bank (SI) and Silicon Valley Bank (SIVB). Both of these companies had issues leading up to this, but the real trouble of course happened when it finally came time to sell their debt.

For Silvergate, the trouble started back when FTX went under in November (hard to believe that was only 4 months ago!). Of course, that event caused a panic and depositors rushed to withdraw their money: a classic bank run.

As you probably know, banks don’t keep all that cash on hand. They invest a lot of it in safe assets like Treasury bonds, and that’s exactly what Silvergate did. The problem was that they loaded up on debt during the “cryptomania” of 2020/2021, when rates were basically nothing.

So, they had a lot of debt paying 1% interest in a market where anyone can go buy Treasuries and earn over 4% per year. Selling all that debt at market prices (which was how their balance sheet listed it) was a pipe dream.

Instead, they had to lower the price significantly, because nobody wants debt that pays them a quarter of what current Treasury bills pay; this resulted in Silvergate taking a $1b hit in less than a month, wiping out their profits for the prior 8 years.

Now, nobody wants to bank with someone who may not be able to return their funds. As a result, insolvency rumors have a high fatality rate for banks, and Silvergate at that point was as good as dead, as their share price reflected. Earlier this week, they officially liquidated, ending a several-month-long death spiral.

Now, let’s talk about SIVB.

This is a much bigger and more reputable bank, and most of their business is comprised of loaning out money to Silicon Valley VCs.

After the past couple years, a lot of huge bets on startups haven’t panned out, and so their $15b loan book to early stage companies has been seen as somewhat of a bruise on the company. In reality, this was nothing too serious as it was only 21% of their total loan portfolio.

The real trouble came earlier this week when they announced they sold their entire “available for sale” securities holdings for $21b…which is a lot of money, but they also took a $1.8b loss on the position because of the lack of demand. The craziest part is, that really wasn’t THAT bad for SIVB; their total asset portfolio was sitting at about $200b. But two things happened.

1.) People questioned how much that $200b was actually worth

2.) People lost faith in the bank and pulled their money out – another bank run

This is another wild example of how loss of faith can lead to a bank with a valuation of $15.8b being shut down by the state of California in less than 48 hours.

The purpose of this article isn’t to scare everyone, it’s to put into perspective how much damage rate hikes of this magnitude can do.

What happens next? Defaults.

The original point of this article was going to be on the looming danger of corporate defaults setting in later this year, but considering what happened with Silvergate and SVB, I had to include their situations as well. This is why I’ve been saying for about a year now that a lot of the “safety” stocks that rely on debt to fund not only their operations but also frivolous things like share buybacks and dividends are not safe at all.

This is also where we need to be particularly careful about growth stocks. A lot of growth companies set projections a couple years ago, but in reality, they’ve fallen way short. If they funded themselves primarily with debt, that’s a big issue as it makes them less reliable to lend to.

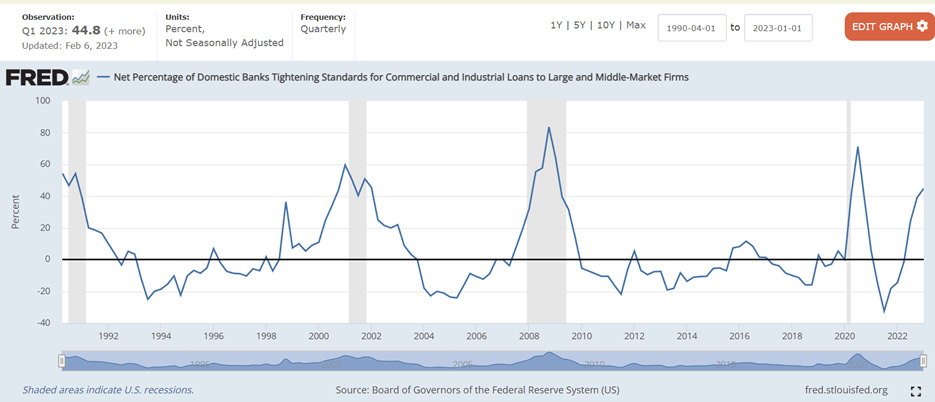

And as we can see here, banks have been extremely cautious with who they choose to lend to in recent quarters:

That chart shows that 44.8% banks are tightening their lending standards for loans to large and mid-sized companies, which are typically safer to lend to.

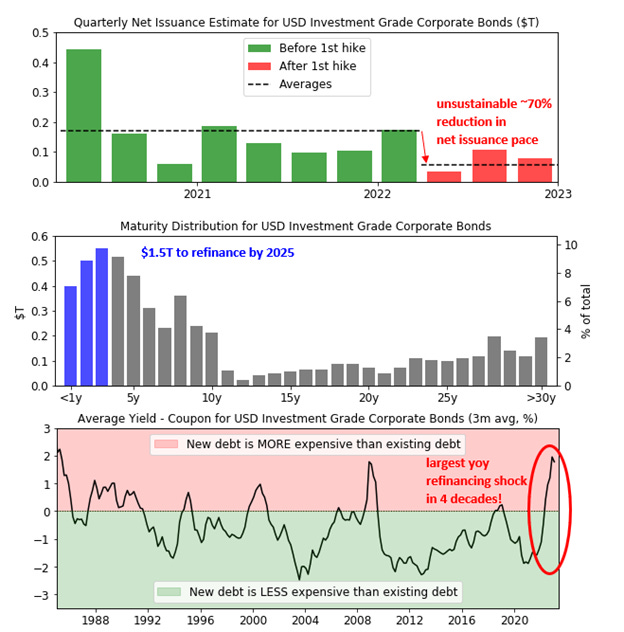

On top of that, there’s about $1.5 trillion that needs to be refinanced between now and 2025, and about $400b of that is due in less than a year:

Companies have gotten accustomed to refinancing or issuing new debt at the drop of a hat for basically no cost. However, it’s a totally different picture now. Not only are rates on new debt way higher, but also banks are much more particular with who they lend to.

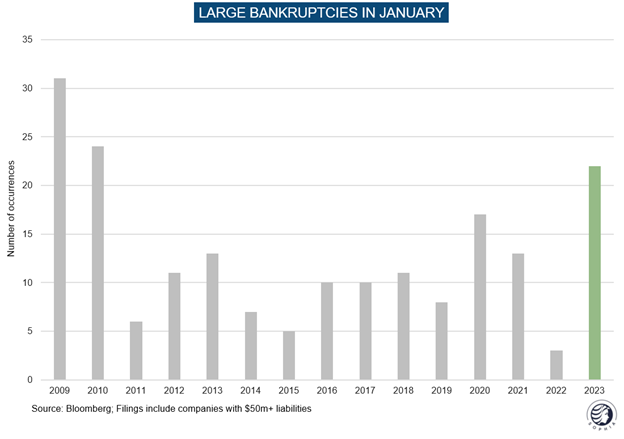

We actually saw some early signs of this in January:

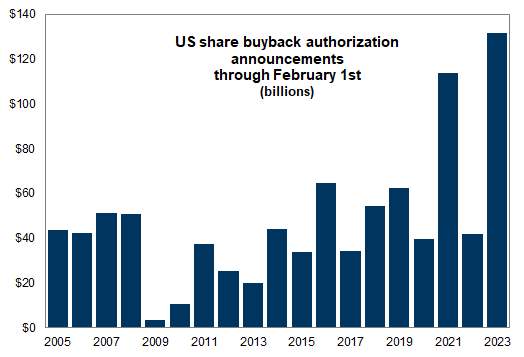

Companies seem to be blissfully ignorant to this as they continue to raise their dividends and announce more share buybacks. Or should I say: “record high share buybacks:”

While I do think those things are usually a dumb use of money, it makes it exponentially more dangerous if they’re funded by debt.

Either way, the first dominos have fallen with Silvergate and SVB. So, what now? A few thoughts on what will unfold from here:

Old habits die hard. traditional investors will keep flocking to “safety” stocks out of fear and willing ignorance (they get fired if they don’t follow the crowd – especially during a panic). And they’ll probably get crushed.

The Fed won’t care until it’s too late. They didn’t care about Bear Stearns and didn’t even bail out Lehman Brothers. Silvergate and SVB can easily be written off as a “fringe event” caused by “highly speculative investments” like crypto.

The Fed does not care about SVB, whose market cap of $15.8b pre-crash was about ¼ of Lehman’s 2007 market cap of $59b. Keep in mind that the 2020 Fed action came as a reaction to a literal global lockdown – this is nothing remotely close to that, and it’ll take a lot more for them to act.

On a related note, stimulation to the economy right now would drive inflation back up; if not immediately, it would likely flare up again within a year as we saw last time:

Bitcoin will eventually benefit from this, just not yet. If the Fed miraculously lets these dominoes fall, Bitcoin could permanently stop trading as a risky asset. It’s been my thought for a while that it’s going to take a major event to kickstart that decoupling process, so we’ll see how far this contagion spreads. And more importantly, how long it’s allowed to spread. The longer, the better. It won’t be pretty short-term, but it would absolutely drive massive Bitcoin adoption.

It’s more important now than ever to be a stock picker. Companies that have low debt, lots of cash, positive cash flow, and a disruptive business are extremely underrated and the market will correct for this at some point. When? I wish I knew!

Not all growth stocks are good. There are a lot of companies that fit into the “growth” category. SI and SIVB fell into this category. CVNA falls into this category. OPEN falls into this category. Two of those are now gone, and the other two are on life support with minimal chance of survival. There are plenty more like this.

First and foremost, staying away from debt-heavy companies is crucial. And within the debt-light companies, it’s preferable to find ones that aren’t regularly issuing shares and diluting the supply. The right balance of growth, debt, cash, disruption, and ability to meet expectations creates a sweet spot that will ultimately win. That’s what I’m aiming to find with my 21 Disruptors Index, which you can find here.

Next week, be on the lookout for the next earnings update where I go over Q4 earnings for PLUG, DM, UUUU, and DOCU. Spoiler alert: I’m starting to lose patience on PLUG, and might be removing them from the list soon.

Disclaimer: Everything presented on my Substack is based on my personal research and opinions, and it should never be taken as investment advice. Just because I say good things about a stock or crypto or any investment doesn’t mean it’ll go up (although I wish that were the case). Any action that you take after reading anything on my Substack is your own responsibility.

Ian PLUG's earnings slides were very impressive! Did you see those?