The Fed Is Getting What They're Looking For

The Fed Is Getting What They're Looking For

But They're Looking In The Wrong Places

I’ll start this week by going over today’s FOMC meeting, and then getting into a couple macro data points that came out last week: the Leading Economic Index (LEI) and GDP.

FOMC:

As pretty much everyone expected, the Fed decided to hike the Fed Funds Rate by 0.25% for the first meeting of 2023, down from a series of 0.75% and 0.5% hikes in 2022.

There are two things that were said during this meeting that I want to highlight.

1.) “Ongoing rate increases will be appropriate”

Every Fed meeting, there seem to be rumors that the next hike will be the last. This one was no different, but it looks like Powell is leaving the door open for more hikes. That makes sense considering what data the Fed looks at; Powell pointed out that the job market is still strong, and inflation is still well above the 2% goal, both of which suggest the economy can withstand more pressure.

There’s actually a futures market for the Fed Funds rate that shows the projected level for each month. Right now, rate expectations peak in June at about 4.88%, which means there’s still 1 more 0.25% rate hike priced in.

Regardless, the Fed has now raised the Fed Funds Rate by 4.5% in less than a year. At this point, I don’t think it’ll matter much whether they do a couple more 0.25% rate hikes or not.

2.) “The disinflationary process has started”

This is definitely true when you look at the price of goods and energy, as I’ve shown many times. The Fed uses the CPI and PCE, and their favorite metric is Core PCE, which excludes food (still very inflationary) and energy (has been deflationary for 6+ months).

Core PCE was up 1.82% in the 2nd half of 2022, after being up 2.55% in the first half of the year. So, it’s definitely deflationary, but still not close to the 2% annual target the Fed is looking for.

There’s a theory out there that the Fed will back down and stop hiking if inflation goes down to 3% or 3.5%, but by saying that ongoing rate hikes are necessary, the Fed is clearly pushing back on that idea.

Overall, Powell seemed relatively upbeat and encouraged by how inflation has been coming down while the job market stays strong. However, both of those things are lagging indicators, and we can get a much clearer picture on how strong the economy is by looking at many other pieces of data. And there’s a lot of data that suggests that by the time the (official) employment picture gets bad enough to start to cut rates, there will be serious issues with the economy in general. Last week, we saw this trend get even stronger with the LEI and GDP data.

LEI:

Last Monday, Conference Board released their leading, coincident, and lagging December economic indices. As you probably noticed by how much I talk about these, I find them some of the most useful tools out there. So, how did each one perform in December?

The leading economic index was down 1% for the month, and is now down 3% over the past 3 months.

The coincident index inched up by 0.1% in December, and is now up 1.4% over the past 6 months.

The lagging index was up 0.3%, which is a slower trend than its total increase of 2.4% over the past 6 months.

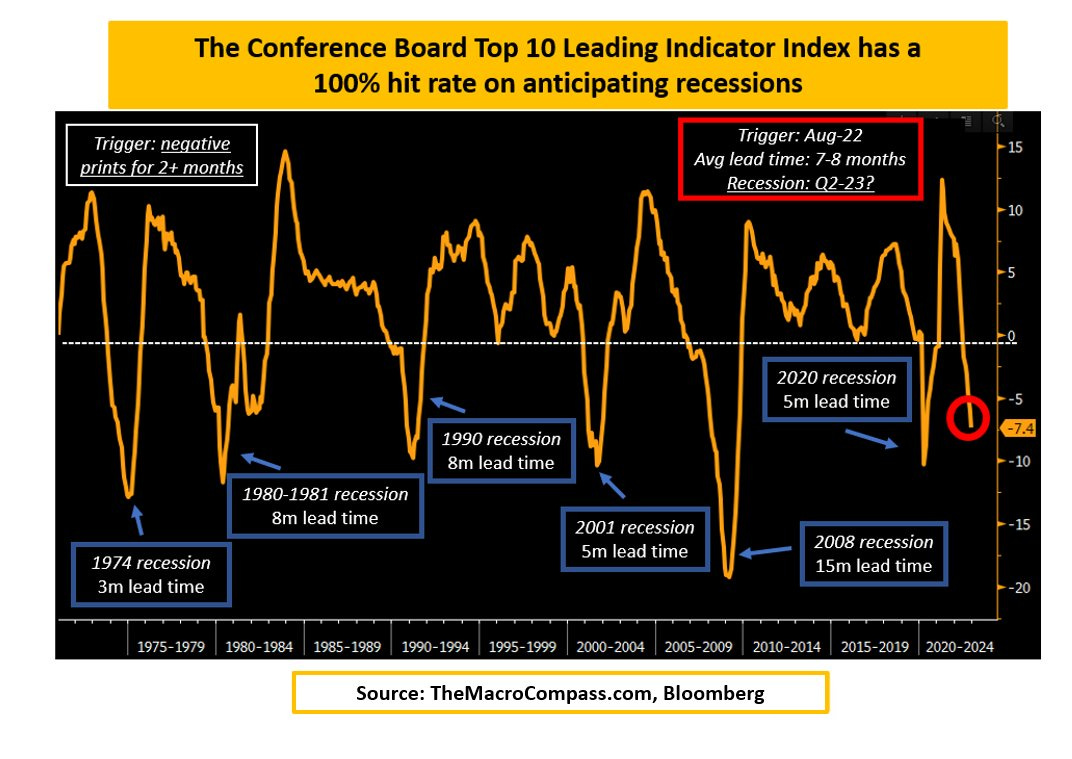

This chart shows the annualized move in the LEI based off the past 4 months; when it flips negative, a recession usually happens within the next year.

It went negative in August, and in my opinion we’re still at least 3-6 months out from a legitimate recession. Of course, it’s never a good idea to dogmatically follow a chart just because it’s predicted things before. However, evidence continues to accumulate that the economy is seriously weakening.

As I’ve shown in the past couple articles, new orders are down significantly in recent months, and retail spending was exceptionally weak during the holiday season. Both of these are solid coincident indicators. Additionally, we’re seeing increased layoff activity in recent weeks, which we’ll take a look at later.

The next stage that will unfold as we move through 2023 is corporate earnings, which I’ll be covering each Friday for the next month or so.

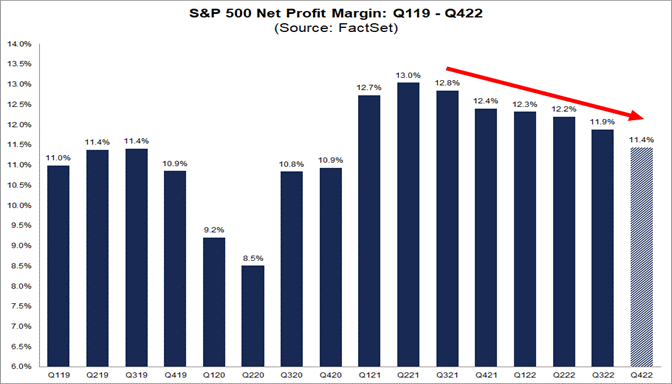

Total EPS of the S&P 500 went parabolic in 2021 and 2022 due to tons of economic stimulus. However, it looks like we’re at the tail end of this now, and things should start reverting back towards 2019 levels for a lot of the bigger companies.

In 2022, margins for a lot of companies declined, which you can see in this chart:

And profit margin expectations for 2023 have been in freefall in recent months, moving down from about 13.5% to 12.4%

GDP:

On Thursday, we got the official GDP data that showed that the economy expanded at an annual rate of 2.9% in Q4. However, like most headline data, the overall number for GDP can be extremely misleading.

This was true last year when everyone was saying we were in a recession after GDP fell for 2 quarters, even though the criteria for recession weren’t really there. The same holds true today, as last week’s 2.9% growth reading looks good on the surface, but any digging will reveal the underlying weakness.

To give a high-level overview, GDP is constructed from 5 main parts: consumption, private fixed investment, private inventories, government spending, and net exports. Here’s how each one contributed to the total 2.9% in Q4:

Consumption: +1.42%

Investment: -1.20%

Inventories: +1.46%

Government spending: +0.64%

Net exports: +0.56%

Note that the only negative component on this list is investment, which almost cancels out the effects of consumption in Q4. Investment includes the amount spent on lots of big-ticket items like housing, durable goods, industrial equipment, etc., which are some of the most important things to look at when gauging the state of the economy. These are included in the “fixed investment” portion of GDP.

In Q4, fixed investment was down an annualized -6.7% QoQ, which means that demand for big-ticket items plummeted. This is in-line with the data we’ve seen in recent months that says new factory orders are down, inventories are high, and backlogs are shrinking. In other words, companies are fully stocked, and due to macro conditions, orders are slowing – the same thing that a lot of industrial and chip companies have been saying for the past couple quarters.

As new orders slow, it means companies in in the goods economy are facing hardships as they’re overstocked with inventory. As expected, a lot of these companies are going to have to drop their prices, which brings us to the underlying theme that ties everything together: deflation.

The Effects Of Deflation

As inflation continues to cool off and eventually turn to deflation, it’s not only going to impact the margins as we showed earlier, but also the top-line sales.

Deflation also means that companies’ input costs and prices will fall, but one expense that won’t fall is wages. Unsurprisingly, it’s a lot harder for companies to tell people that they have to take a pay cut than to give them a raise, and a lot of companies will be forced to lay people off. This has been the case for a while in the land of tech and startups, but it’s now happening in other industries as well. Here are some examples:

Hasbro is laying off 1,000 people (15% of workforce)

Dow Inc is laying off 2,000 people

Ford is laying off 3,200 people

3M is laying off 2,500 people

Vacasa is laying off 1,300 people

Capital One is laying off 1,100 people

Wayfair is laying off 1,750 people

Genpact is laying off 1,000 people

Philips is laying off 6,000 people

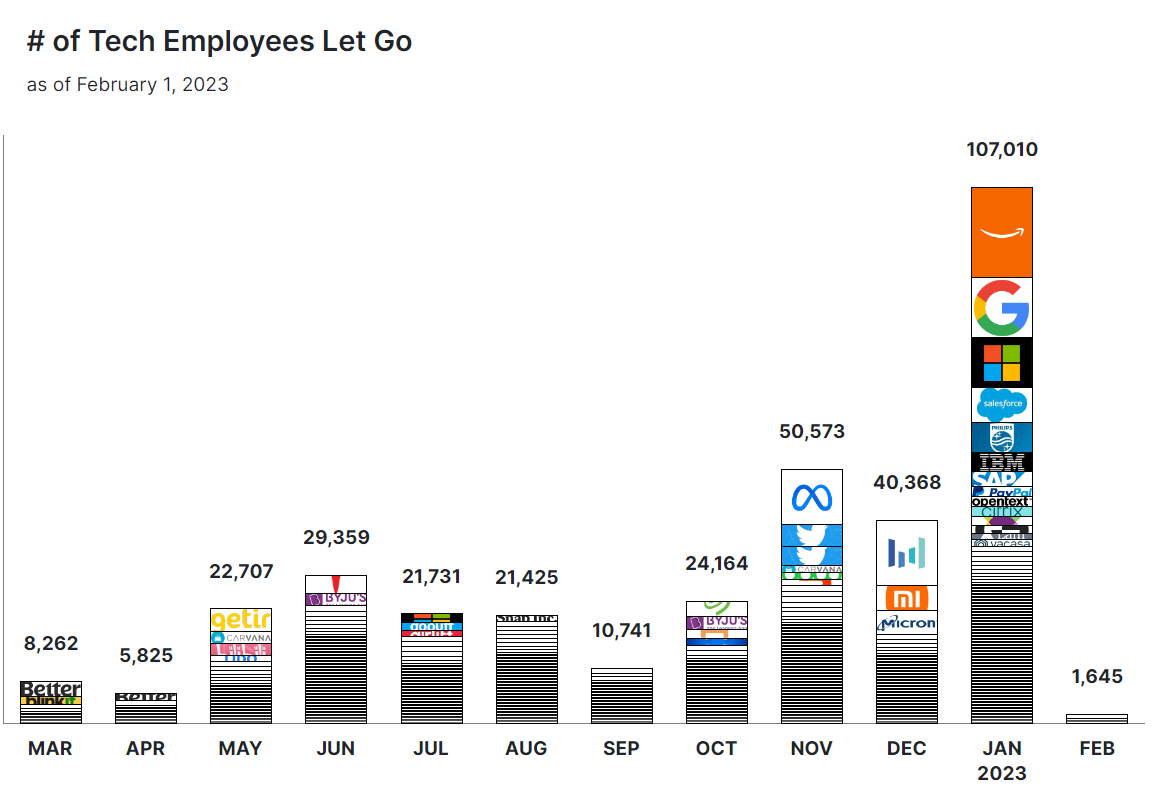

In addition to that, the layoffs within tech are getting bigger and more frequent. For example:

Paypal is laying off 2,000 people

Google is laying off 12,000 people

SAP is laying off 3,000 people

Lam Research is laying off 1,300 people

OpenText is laying off 2,000 people

IBM is laying off 3,900 people

All of the layoffs I just listed, tech and non-tech, have happened in the past 12 days. To visualize this trend, you can see here that January saw a major increase from recent months, with over 107k layoffs announced:

If margins continue to deteriorate as expected and sales slow at the same time, that’s going to be a double whammy on earnings in 2023, which will result in more layoffs, which will result in less consumer spending, which will result in further deflation, and the cycle continues.

As I’ve been saying for months, this was to be expected as margins get tighter for companies across the board. It’s also going to continue outside of tech, mostly in the sectors that rely heavily on durable goods. One thing I’m interested to see over the span of 2023 is how design/simulation stocks like PTC and CDNS, as well as 3D printing companies like PRLB and DM hold up. In recent earnings reports, the design/simulation stocks have sounded much more positive about the current demand landscape, while 3D printing companies, despite their next-gen technology, haven’t been able to escape the tightening global conditions (meaning demand has gotten worse for them, too). PTC reported after the close today, and you can expect a thread on Twitter from me tomorrow morning to cover their earnings report.

Now, I assume that the Fed will pivot if we see a big spike in unemployment, but it's hard to say exactly how that will play out, or how much damage will already have been done at that point. The relief efforts that sent the economy into overdrive in 2020 and 2021 were some of the most extreme measures taken in US history, and it would take a lot to see a repeat of that. After all, it’s those policies that drove the Fed to raise rates at an unprecedented pace – from 0% to 4.25% – last year. It’s why the economy seems so resilient, and it’s why the Fed’s tightening will likely prove to be too much later this year. For now, it’s been contained to leading indicators, but towards the end of Q4, we saw it bleed into coincident indicators like industrial production and retail sales.

If we do see the S&P 500 make new lows (I know it’s hard to imagine at this point, but I’m still expecting it), it will be very interesting to see how the quality growth companies like the 21 Disruptors hold up in terms of share price. A lot of these companies have been surprisingly resilient thus far from a business standpoint – they’re still taking market share, seeing solid revenue growth and cash inflow, and doing what they do best: innovating. If deflation does play out as I expect, and a lot of debt-heavy, labor-heavy companies suffer, the revenue growth, high cash balances, and low debt burdens that the Disruptors have to offer will be seen as a scarce resource in a market where sales, margins, and profits are all down.

Right now, that appears to be the clearest path forward for 2023, and it will surely be interesting to watch how it all plays out.