Two 3D Printing Stocks For Big Gains

Two 3D Printing Stocks For Big Gains

As countries look for solutions to become economically self-reliant, these two 3D printing stocks are my picks for the coming manufacturing revolution.

· Overviews of Desktop Metal and Proto Labs (0:00)

· 21 Disruptors Index Update (4:51)

· Why to Watch Wage Inflation (7:31)

· How the Job Market Keeps Getting Stronger (8:07)

I’ve said it before and I’ll say it again: 3D printing is my favorite sector to invest in. We haven’t seen technology this disruptive in manufacturing in a very, very long time.

Sure, stocks in this industry have been struggling, but I want to start off this week by going over two of my favorite 3D printing plays for the future.

Of course, these are also included in my new 21 Disruptors Index. If you haven’t seen the full 21-stock list, I go over it in last week’s article.

3D Printing: The Way to Play the Onshoring Trend

3D printing is essentially a bet on deglobalization and onshoring. That basically means that countries are going to have to be more self-reliant. Over and over during the past few years, we’ve seen what can happen when you’re too reliant on other countries to give you vital goods.

Of course, one of the biggest arguments for globalization was the fact that you could outsource your manufacturing to other countries to take advantage of cheaper wages. However, that means that bringing production back home would mean higher prices; that’s something we don’t want to see when inflation is already rampant.

The only way to offset the higher wages you’d be paying workers at home is by cutting the costs of actually producing things.

So, as onshoring finally gains momentum, I see 3D printing as one of the most obvious bets in the market right now.

Within the manufacturing sector, Desktop Metal Inc. (NYSE: DM) and Proto Labs Inc. (NYSE: PRLB) are our two 3D printing plays. I picked these two because they have very different business models.

The Stocks

Desktop Metal is one of the most innovative publicly traded 3D printing companies I’ve come across.

As the name suggests, their main focus is on dominating the market for 3D-printed metal parts. This is a technology that’s been riddled with speculation for decades, but it’s finally becoming a reality.

More specifically, 3D printing has been (for the most part) used to create prototypes of actual products. That’s not a bad thing. In fact, the ability to 3D print cheap prototype/test parts is very useful.

However, it’s also very limiting compared to the magnitude of mass production, which is where Desktop Metal is taking the industry forward.

Earlier this year, they began shipments of their flagship “Production System P-50.”

The P-50 was described in their most recent earnings call as “the fastest metal printer in the world,” which “makes parts 1/20th the cost of competitive alternative systems.” The CEO also remarked that over 90 companies have already made a down payment for their own.

Desktop Metal’s success is evident when you look at their sales, which have gone from $16.5 million in 2020 to $183.5 million over the past year — an increase of 1,012% in less than two years!

Another reason I like Desktop Metal so much is that they have loads of cash.

You’ve probably heard me say this many times by now, but I believe the stocks that’ll come out stronger on the other end of this bear market will be those with healthy balance sheets. In essence, that means lots of cash and little to no debt.

This is certainly the case with Desktop Metal, as they have $255.7 million in cash versus just $111.9 million in long-term debt.

Proto Labs is focused on becoming the biggest and best online 3D printing marketplace. Essentially, this is where you go if you need to order any type of 3D-printed object, from plastic prototypes to sheet metal for a new airplane.

The most exciting thing going on right now at Proto Labs is their Hubs platform, which they acquired back in early 2021.

Hubs essentially connects the customers of Proto Labs with 240 manufacturers in 20 different countries, so that orders are immediately priced and routed to the right manufacturers for the job.

This acquisition probably accelerated their business by years and put them at the forefront of their market.

Before the acquisition, they mostly focused on custom parts, which is, of course, a much smaller market. But because of the resources that they’ve gotten via Hubs, it’s much easier for Proto Labs to fulfill huge amounts of orders for a wide variety of products.

And with 3D printing still being a relatively niche market, if you can have a business that merges quality with variety, you’re set.

With Hubs, Proto Labs has one of my favorite things to see in an investment: a relatively small part of their business (only 8.9% of their current revenue) that’s growing rapidly and representing a huge part of their future.

Proto Labs’ stock price tells me that the market seems to be ignoring or overlooking the value of a global 3D printing online marketplace.

Considering that 3D printing is becoming increasingly relevant in the wake of a worldwide reshoring effort, I’m more than happy to take that bet.

Weekly Recap

Each week, I’m going to show the performance of the Disruptors Index vs the S&P 500, Nasdaq, the Russell 2000 and Ark Innovation Fund, as well as go over the top performers in the Disruptors Index.

The first week for our Disruptors Index was a rough one, but it still outperformed the major indices as well as ARKK.

21 Disruptors Index: -2.77%

S&P 500: -2.97%

Nasdaq: -3.73%

Russell 2000: -4.71%

ARKK: -4.84%

Top 5 Performers:

Guardant Health Inc. (Nadsaq: GH ) +6.1%

Enphase Energy Inc. (Nasdaq: ENPH ) +2.47%

Ethereum (ETH) +2.12%

Airbnb Inc. (Nasdaq: ABNB) +1.01%

Pinterest Inc. (NYSE: PINS) +0.64%

Bottom 5 Performers:

MP Materials Corp. (NYSE: MP) -9.4%

Energy Fuels Inc. (NYSE: UUUU) -8.98%

Plug Power Inc. (Nasdaq: PLUG) -8.3%

DocuSign Inc. (Nasdaq: DOCU) -8.14%

Teladoc Health Inc. (NYSE: TDOC) -6.69%

Keep an Eye on Wage Inflation

Within all the speculation of inflation and what the Fed will do in order to tame it, I think one huge thing is being overlooked: wage inflation.

Just about every company has felt the burn of higher energy prices over the past year. Whether you’re in retail, manufacturing, or financial services, you rely heavily on fuel and/or electricity to make your business run smoothly. Thus begins the cycle:

1) Higher input energy costs mean it costs more to make things.

2) When it costs more to make things, companies need to raise prices.

3) When companies raise prices, people need to spend more.

4) In order for people to spend more, they need to be paid more.

5) When companies are forced to pay more, it costs more to make things.

6) Step 3 of the cycle repeats.

The two major inputs costs for any business are capital and labor. When capital costs (in this case, energy) are high for an extended period of time, it inevitably leads to labor costs going up as well.

So far, we haven’t seen labor costs go way up. In fact, average inflation-adjusted wages in July of this year were about 3.6% lower than they were in July 2021.

This is in spite of one of the most interesting trends in the overall economy. For over two years, more and more people have been quitting and changing jobs. We know that the labor market has been strong, as there are almost twice as many job openings as there are unemployed people looking for work.

What’s even more impressive about that strength is the fact that people have been quitting their jobs in record numbers. Last year, a record 47.8 million people quit their jobs, and in 2022, we’re on pace for about 51.6 million.

This is a positive sign for the job market because it means that people presumably are easily able to find better jobs. Not only that, but they’re also making a lot more money as a result.

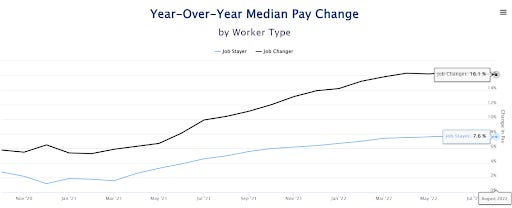

As you can see here, “job changers” have seen a 16.1% increase in pay over the past year, as opposed to “job stayers” who have only seen a 7.6% increase on average — below the rate of inflation.

Source: ADP Research Institute

Basically, if an employer’s pay rate isn’t keeping up with inflation, their employees are switching to companies who can keep up. In other words, they’re following the money.

Obviously, this is a good thing for employees. The question I have is: How long is it going to be sustainable?

Margins: At a Tipping Point

Last quarter, I stressed the fact that certain areas of the economy were seeing higher expenses take a toll on their profitability. Most of the damage so far was dealt to retail companies like Target, Home Depot, and Wal-Mart.

However, this problem is going to hit more sectors going forward if energy costs remain relatively high and labor costs go up.

That’s because at the same time as they’re paying higher costs for labor and energy, they’re having to cut prices on things they sell, so they’re bringing in less money per item while paying higher fixed costs.

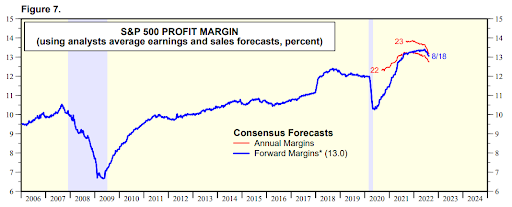

As you can see in this chart, profit margins are expected to move down through the end of 2022 into 2023.

Source: Yardeni.com

The line that catches my attention the most in this chart is the top red line, which is the profit margin estimate for 2023.

Until recently, analysts were very confident that we’d see profitability continue its move upward to new highs. But within the past few months, their estimates have come down by almost 1%, which is actually pretty significant.

On one hand, this is to be expected since margins are still very high. However, if labor costs keep moving up faster and faster, those margins will come down quicker as well.

Growing Labor Force

So, the ongoing trend continues: People are quitting their jobs in record numbers because they know they can make more money elsewhere.

This is a sign of strength for the job market, but as inflation stays high, companies who are raising wages faster than inflation will eventually hit a wall.

However, there’s another trend beginning to form which could accelerate this process, causing a potential disruption in the job market…

Last Friday, unemployment data came out that caught my eye: In August, the number of employed people went up by 442,000 and the number of unemployed people went up by 344,000 (a net increase of 98,000 employees).

But at the same time, unemployment was somehow up 0.2%.

The reason for this is actually simple: A ton of people entered the labor market last month — 786,000 to be exact.

What I get from this is that it’s a somewhat-delayed reaction to a very strong job market, where people who had been laid off as a consequence of COVID lockdowns are now re-entering the job market.

What does this mean? Over three quarters of a million people in one month is no small amount, so how many more people are going to re-enter the job market? And what does that mean for inflation?

Well, if we go back to the job market pre-covid, we can get a better idea of this.

The number that really matters here is the “civilian noninstitutional population,” or CNP, which is just a fancy way of saying the total number of people who can potentially be employed.

Since February 2020, this number has increased by about 4.56 million people.

At the same time, the labor force — which is the portion of the CNP that’s looking for work — has only gone up by 142,000 people.

We potentially have the beginning of millions of people returning to the job market.

There are two ways this can go…

Scenario 1: Demand for labor stays high.

People will be able to seek out higher wages easily, and businesses will have to keep increasing their pay to satisfy workers (until they can’t anymore — and in the meantime, they’ll have to keep increasing the cost of their products to offset the higher wage expenses).

Scenario 2: Demand for labor goes down.

Too many people enter the labor market too quickly, and companies can’t afford to hire as many people as they had thought.

I think Scenario 1 is the most likely to happen for at least four to six months out. After that, it’s very dependent on energy costs and demand from consumers.

In the best-case scenario, demand for labor stays high as the cost of energy comes down. Some of the bigger retail companies would still go through a rough period, but much of the potential hit to the economy would be avoided.

To sum up, inflation of energy and commodity prices has certainly cooled off during the past couple months.

Next, we need to be very aware of wage inflation, which is a factor that could potentially keep prices higher for longer than expected.

Because the job market is still so strong, employees have more pricing power than employers, which means it’s relatively easy to find jobs that’ll increase your pay at a higher rate than inflation.

As people make more money, they’ll most likely spend more … and as companies pay higher wages to make their jobs more desirable, they’ll need to raise prices. Both of these forces are inflationary.

Ideally, we’ll see commodity prices — especially energy — move lower, and this is certainly something to keep a close watch on.

If you enjoyed this Substack, please consider subscribing!

Where do you stand on the 3D stock in Profits unlimited?

Ian, I really like your writing’s because they’re to the point, full of information but not to lengthy. I can tell you really know how to do your homework. 👍