What We Learned Last Week About The Economy

What We Learned Last Week About The Economy

Diving into the PMI reports for goods and services, which are a great gauge for the overall pulse of the US economy

If you’ve been following my Substack for the past few months, you’ll be familiar with the concept of leading, coincident, and lagging indicators. Understanding which data point is which is crucial for understanding the state of the economy. Otherwise, you’ll get caught up in narratives like “the jobs market is strong, so the economy is strong.” While there’s some truth to that, if you’re waiting for the job market to go south before you can officially say the economy is in bad shape, you’ll be extremely late to the game.

As a reminder, here’s an overview of the biggest indicators in each category:

Leading: building permits, consumer business expectations, mortgage applications

Coincident: purchasing managers’ index (PMI), factory orders, corporate profits

Lagging: unemployment, CPI

For most of 2022, a lot of leading indicators began to crumble, and then nosedived in the second half of the year. We’re now seeing early signs that coincident indicators will do the same thing over at least the first half of 2023.

Last week had a few key coincident indicators that are beginning to paint the picture, namely the PMI data that I mentioned above. The Institute for Supply Management (ISM) posted their monthly data on the state of the manufacturing (goods) economy and the non-manufacturing (services) sides of the economy.

We’ll go into some of the details, but as a broad overview, the ISM boils a ton of different data points down into a final number. If that number is over 50, it means that part of the economy is expanding; if it’s under 50, it means it’s contracting.

The State Of The Goods Economy

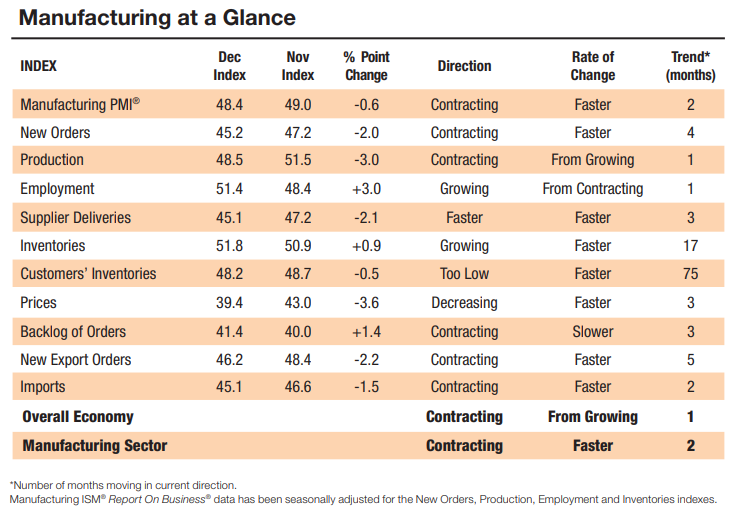

On Wednesday, we got a view into the “goods” side of things with a final PMI number of 48.4. That means the manufacturing economy is in contraction, which should be no surprise as we’ve seen auto, appliance, and retail inventories pile up for the better part of a year.

The manufacturing PMI data topped out at 64.7 all the way back in March 2021, and it was a slow road down until it finally broke below 50 in November 2022:

If we look at the components of what give us that 48.4 number, we’ll get a better sense of where the weakness lies:

Source: Institute for Supply Management

It probably goes without saying that the rows marked as “contracting” and “faster” are the worst parts of the manufacturing economy. In that category, we have:

New Orders – 45.2

New Export Orders – 46.2

Imports – 45.1

Exports and imports are signaling the global trade is slowing down at a faster pace, which should also not be a surprise as Europe and Japan are in an even worse position than the US, and China is still bogged down by lockdown effects.

Domestically, new orders are down as well, as a lot of companies over-ordered during the reopening phase and now have way too much inventory.

Side note: we also got the Factory Orders data for November on Friday, which fell 1.8% from October – the largest monthly decline since October 2018 (other than the covid lockdowns).

The effects of that inventory buildup can be seen in “prices,” which is the lowest number on the list at 39.4. Goods have been deflationary for a while now, but a lot of the CPI measures the price of services so we haven’t seen the goods deflation in the “official” numbers. However, this will continue to have a bigger and bigger effect on the CPI over the coming months.

The lone positive in this report was the employment component, which flipped into expansion territory in December, coming in at 51.4. However, like I said earlier, employment is a lagging indicator, and this has been hovering around 50 for a while now:

The State Of The Services Economy

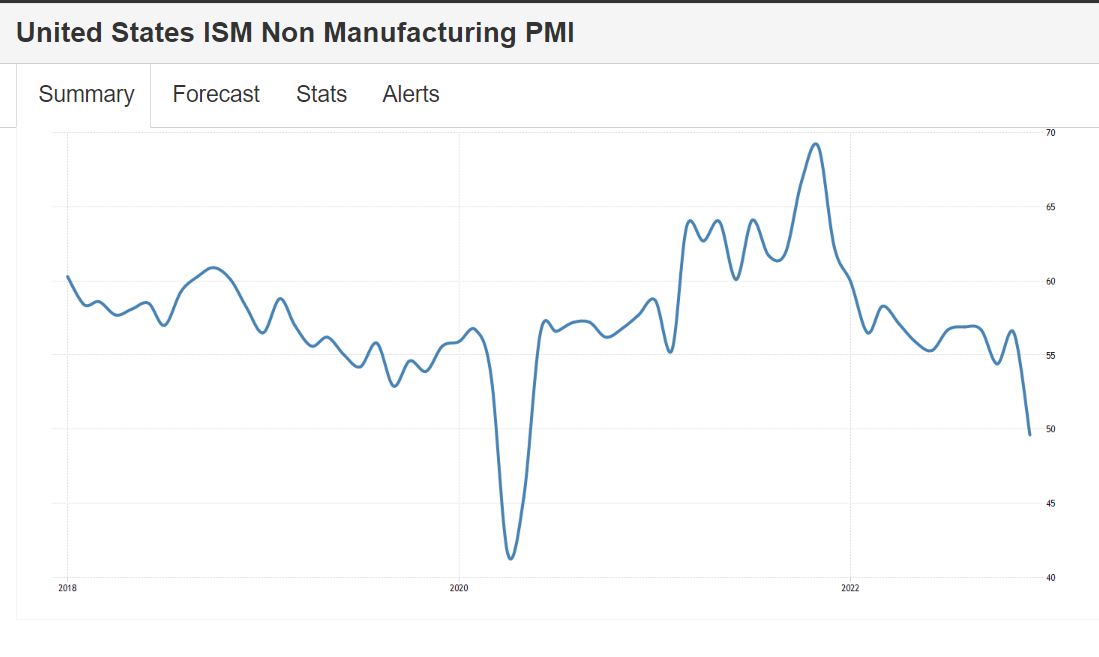

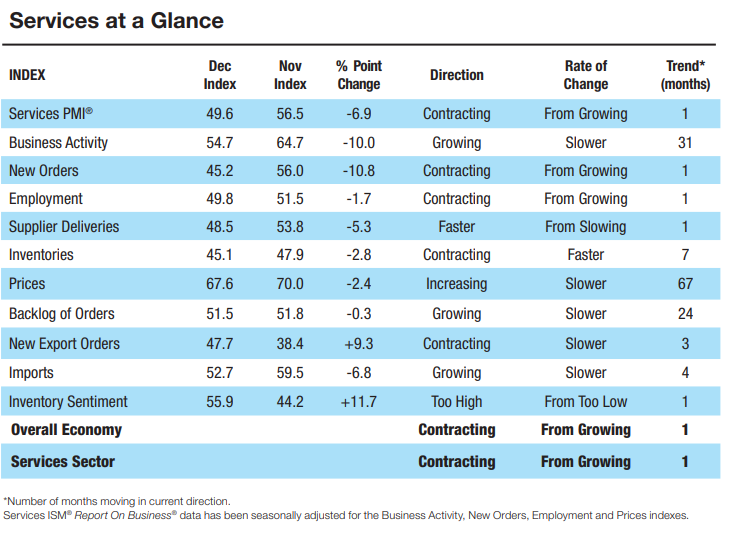

On Friday, we got to see into the other half of the economy: services. The ISM non-manufacturing PMI came in at 49.6, which suggests that the services economy is also in contraction.

This was a much bigger surprise than the contraction in the goods economy, as the official forecast for December’s services PMI was 55, which is still well into expansion territory. In fact, other than the covid crash, this was the worst non-manufacturing PMI reading since January 2010.

The services economy has been an increasingly important part of the overall economy for the past couple decades as the US has become reliant on other countries for manufacturing, and consumer preferences have shifted from goods to services.

Ultimately, if this stays low, it’s a huge recessionary signal. Here’s a look at the components for the December services PMI:

Source: Institute for Supply Management

Overall, there are four different components in contraction territory:

New orders – 45.2

Employment – 49.8

Inventories – 45.1

New Export Orders – 47.7

Based on the new orders and new export orders data, we can see that demand both foreign and domestic is slower than it was in November. The domestic demand is the worse of the two, though, as it took a huge plunge from November’s reading of 56 all the way down to 45.2. Export orders were contracting, but not as badly as in November, when the reading was all the way down to 38.4.

Employment dipped slightly into contraction, but like the goods economy, this has been straddling 50 for a while now:

The main difference between goods and services is inventories, as services inventories are actually contracting

Lastly, if you look at the “prices” component, you’ll see where a lot of the CPI is coming from. Even though this number went down in December, it’s still very expansionary at 67.6, meaning services prices are still highly elevated. We’ll get more detail on this on Thursday when December’s CPI data is released, and I’ll have another update for everyone on Friday.

Disclaimer: Everything presented on my Substack is based on my personal research and opinions, and it should never be taken as investment advice. Just because I say good things about a stock or crypto or any investment doesn’t mean it’ll go up (although I wish that were the case). Any action that you take after reading anything on my Substack is your own responsibility.

What is the conclusion ?

Where is the meet ?