2 Ways the Fed Could Pivot

2 Ways the Fed Could Pivot

The Fed is crushing the economy, so there's a good chance a pivot is ahead.

· Performance Update

· U.K. Bond Crisis

· Will the Fed Go Back to QE?

· What This Means for Stocks

I usually start off with an overview of some of our “disruptors,” but considering how much there is to talk about, I’m skipping that this week.

We’ll start off with a performance update for the past week and then get into the pension fund disaster that hit the U.K., whether or not this means we’re headed for quantitative easing (QE), and how this will impact the stock market.

For a quick update, watch the video below:

Performance Update:

Performance:

Disruptor Index: 2.58%

S&P 500: -0.37%

Nasdaq: -0.72%

Russell 2000: 1.25%

ARKK: 0.19%

Top 3 Performers:

Energy Fuels Inc. (NYSE: UUUU) +16.28%

Guardant Health Inc. (Nasdaq: GH) +11.99%

Cameco Corporation (NYSE: CCJ) +8.78%

Bottom 3 Performers:

Tesla Inc. (Nasdaq: TSLA) -11.96%

Teladoc Health Inc. (NYSE: TDOC) -4.08%

Uber Technologies Inc. (NYSE: UBER) -3.95%

Commodity stocks had a solid rebound week as our two uranium plays, Energy Fuels Inc. (NYSE: UUUU) and Cameco Corporation (NYSE: CCJ), were both in our Top 3 Performers for the week.

MP Materials Corp. (NYSE: MP) also had a strong start to the week, gaining almost 6% on Monday after making a few new lows last week.

If you want guidance on similar stocks with promising potential, consider our Platinum Membership, which includes all of my crypto and stock services.

On the other hand, Tesla Inc. (Nasdaq: TSLA) stock had a bad start to the week, and there are a couple possible reasons for this…

Maybe it’s because the company’s Q3 delivery report wasn’t good enough for the market — even though its 343,830 deliveries were 42.5% higher than Q3 of 2021.

On top of that, TSLA now has over 908,000 deliveries for the year, nearly surpassing 2021’s total of 935.95K.

Keep in mind that Q4 has been its top quarter for deliveries for five straight years. Last year, it delivered over 308,000 vehicles, and it’ll be interesting to see just how high they can go this year.

Or maybe the selloff was due to the fact that TSLA’s AI Day over the weekend was yet another buy-the-rumor/sell-the-news event in this bear market.

A general rule to follow in markets is that if a hyped-up event is happening, and everyone knows it, pretty much all the buying will happen leading up to that event, and a selloff will follow (surprising a lot of people who bought).

Either way, the business is booming, as it has been for years … and I don’t place too much importance on a single day of trading — especially on something I see as a long-term investment.

Two weeks from today, we’ll have a deeper look at TSLA’s business strength when it reports Q3 earnings.

U.K. Bond Crisis

Last week, the Bank of England shook things up big time when it reversed course and announced that it’d be restarting QE. Basically, this means that instead of selling U.K. government bonds (also known as “gilts”), it’s now buying them.

When it sells government bonds on the open market, it’s called “quantitative tightening” (QT). Because QT is selling, it creates a lot of selling pressure on gilts, which can drive down the price.

It started a now-short-lived QT program back in March. But now, with the resurgence of QE, it’s acting as a bailout fund. For triviality’s sake, I’d consider this a partial pivot — which will become a full pivot if it begins to lower rates again.

So, why the sudden pivot by one of the most powerful central banks in the world? Well, it turns out it raised rates far too fast and broke something.

That “something” was the $1.6 trillion U.K. pension market, which owned 28% of the U.K.’s debt in Q1. Oftentimes, big funds that are in the asset preservation business have a top priority of minimizing damage, even if it means settling for a very low return.

Government bonds from developed economies are seen as “risk-free,” which means pensions — and other players like them — are actually required to hold a certain amount of them.

So, if these are supposed to be risk-free investments, what happened? How can a risk-free asset be the cause of a financial collapse?

Well, the simple answer is that nothing is actually risk-free.

In this case, almost every major central bank in the world has decided to tighten their monetary systems or raise interest rates and sell off assets like government debt (bonds). This led to two big downward forces on bond prices:

Bond prices and rates have an inverse correlation. So, when rates go up, bond prices automatically go down.

At the same time, the central bank was a huge source of demand for gilts. Suddenly, not only was it not the source of demand anymore, but it did a 180 and began actively selling them on the open market. There wasn’t nearly enough demand to support the prices, so the bond prices faced serious downward pressure.

A global financial tightening like this had never happened before. It was a stress test that’s now exposing some of the cracks in the system.

So, now we know what caused the financial stress in the U.K.: Government bond prices went down way more than anyone thought possible, and the pension funds held a ton of these bonds.

However, another factor made it even worse: margin.

You’d think that something like a pension, whose first priority is preserving capital, would invest in the safest way possible. However, that wasn’t the case here.

In fact, pensions “levered up” on their bond positions, which basically means they spent money they didn’t have to buy them.

This is how margin accounts work. Say you put $5,000 into your account. With margin, you’ll be able to invest something like $10,000, and that extra $5,000 is debt that you’ll have to pay interest on.

Then, if your investment goes down to a point where your original $5,000 is lost, you need to deposit more money.

This is exactly what happened to the pension funds. They loaded up on “risk-free” bonds, which went down way more than they were supposed to, and as a result, the pensions now have to deposit a ton of money (more specifically, money they don’t have) in order to keep their account alive.

The Bank of England had two choices here: bail out the pension funds, or let them fail — meaning millions of people’s retirement income would take a severe loss.

Ultimately, the bank decided to bail them out by doing another round of QE, meaning it’ll buy the pension funds’ bonds for whatever price it needs to in order to keep the funds alive.

While that’s a good thing for a lot of people, it’s going to put the U.K. in a worse position in the long term.

For one thing, it’s most likely going to further weaken the pound. That’s because the Bank of England is buying the debt with GBP, which puts more GBP into circulation, causing inflation. How fast the GBP will make its way into the economy, however, will dictate when that inflation happens.

Overall, I believe this is just another blow to the credibility of central banks. Granted, they’re in a very tough spot, but with every one of these moves, they’re kicking the can down the road.

They went too fast with raising rates — causing bond prices to plummet — and at the same time, sold even more into the market when there were hardly any buyers.

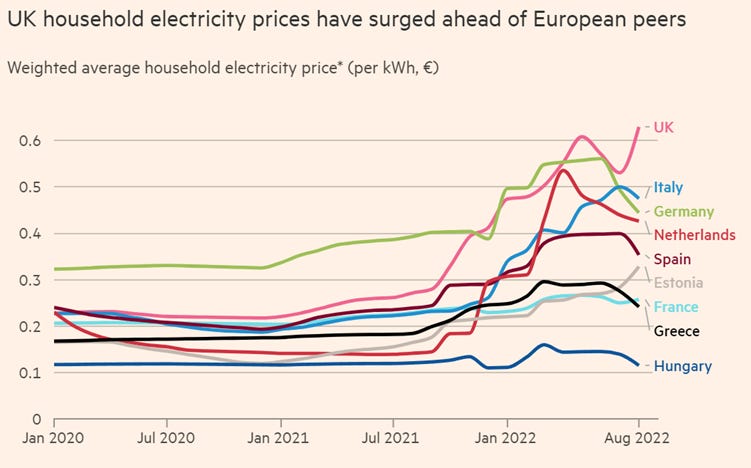

Now, they’re reversing course by buying assets once again, which will stimulate an economy that’s already seeing 9.9% inflation as of August.

The most dangerous areas of inflation are food and energy, as we all rely on both for survival. As you can see in this chart, electricity costs in the U.K. are some of the highest in Europe:

Source: Energy.eu

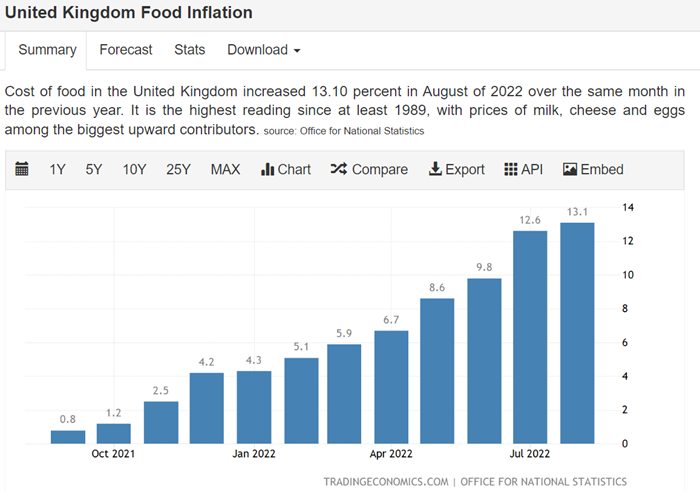

Food inflation in the U.K. also continues to set new highs, with a print of 13.1% in August:

Source: Trading Economics

Obviously, we won’t see the inflationary effects of the QE overnight.

What we’ll see first is the fact that the pension funds don’t default on people’s retirement, which will make it look like a great policy on the surface.

It seems like the QE announcement actually had a positive effect on the pound, as the price has moved up from 1.06 to 1.13 in five days (so far).

But zooming out, it had been in freefall for weeks, and this is likely a short squeeze on the way to lower lows. Easing monetary policy generally doesn’t drive demand for a currency.

What About the Fed?

Let’s take a look at what’s been happening with U.S. Treasuries:

· Yields have soared due to Fed interest rate hikes.

· This has caused bond prices to crash at a historic pace.

· The largest holders of U.S. Treasuries in the world — China and Japan — are selling.

· Since 2008, the Fed has been buying U.S. Treasuries due to QE.

· Now, the Fed is selling U.S. Treasuries.

What we can get from this is that nobody wants to buy U.S. Treasuries right now.

Instead, they want to sell in order to get more USD, which has been outperforming nearly every other global currency this year.

The USD is obviously important to global trade as well. Since most trade is conducted in the dollar, a strong dollar hurts the purchasing power of a lot of countries.

I also think there was so much selling earlier in the year because the Fed told everyone it planned on selling its holdings, and lots of institutions and central banks across the world front-ran their selling, meaning they sold ahead of the Fed.

They knew the Fed would sell, so they wanted to get out before the worst of the selling took place.

Clearly, the Fed isn’t in a good situation here. Bonds have been decimated in 2022, and inflation is still alive and well.

In addition, buyers of Treasury bonds are scarce. As you can see below, liquidity for U.S. Government securities is almost as bad as the COVID-19 crash:

Source: Bloomberg

That’s what happens when the biggest buyer of an asset suddenly becomes a seller!

From here, there’s one huge question that I want to address…

Will the Fed Follow the U.K. Into QE?

My take on this has been that the Fed will begin to pivot (slow the rate hikes down dramatically, but not necessarily stop), either when it sees several months of month-over-month core inflation go down, or if something in the financial system breaks.

With that said, the situation in the U.K. pension market can definitely be filed under “something in the financial system is breaking.”

That can happen here, too, and the idea of a Fed pivot in response to that is definitely plausible.

In that case, it could even be a total pivot, meaning it’d stop hiking rates altogether and cut them immediately.

But just like in the U.K., this would be a temporary solution at best.

Sure, if the Federal Reserve goes back to QE, markets will bounce and people will be happy — but only for the short term. That’s because QE, in an inflationary environment, is asking for trouble.

There have been pockets of deflation here and there, notably in the retail/discretionary areas of the market, as well as automobiles. Of course, energy prices have come down, too, over the past few months.

Previously, I thought that might be a key factor in getting us out of inflation. But as we saw in August, when people don’t have to spend as much on gasoline and electricity, they spend that money on other things.

The fact that the average consumer is extremely tight on cash right now doesn’t seem to matter. As you can see, personal savings is sitting at $652.8 billion, which — other than earlier this year — is the lowest it’s been since March 2010:

Source: TradingView

At this point, inflation has burned through most of people’s savings, resulting in increased credit card use.

Here’s another chart that shows the total ratio of credit card debt to personal savings:

Source: TradingView

From 2010 to 2018, this ratio hovered between 0.8 and 1.2 for the most part. After that, the massive stimulus efforts of 2020 and 2021 pushed it down to 0.2, meaning people didn’t rely nearly as much on credit cards.

And now, the total opposite is taking place. Savings are depleted, and people have to use credit cards to get by. As a result, the ratio spiked over 2 and is now back down to about 1.74.

In other words, people have $174 in credit card debt for every $100 in savings.

I believe this is because of the strength of the job market. As long as people have jobs, they’ll spend money. They just won’t spend as much when the things they need, such as food and energy, suddenly spike in value.

Then, when those necessities drop back down, it’s almost like a stimulus, and the discretionary spending (meaning spending on non-essential items) turns back on.

Will it be enough to prevent mass liquidations from big retailers’ inventories? No way, and that’s definitely deflationary. But it’ll most likely be enough to keep inflation annoyingly high as long as the job market blazes on.

So, unless discretionary spending miraculously goes away very soon, I think there’s only one thing that can result in deflation in the short term: job market pain. And as I explain in this article, I don’t see that happening on a large scale for at least another four to six months.

Because of the persistence of inflation, I don’t think the Fed will join the Bank of England in another round of QE.

In my opinion, it would take something even worse than inflation to cause them to change course at this point.

Would a pension collapse on the U.K.’s scale qualify as worse? Most likely. But right now, any effort to stimulate the economy would open the door for prolonged inflation and more pain later when it’d inevitably have to switch back to QT.

What This Means for Stocks

This all ties back to one thing: liquidity.

During times of panic, investors, companies, and institutions alike rush to cash.

Investors and institutions have been doing this on some level for most of 2022. However, companies have been doing the opposite.

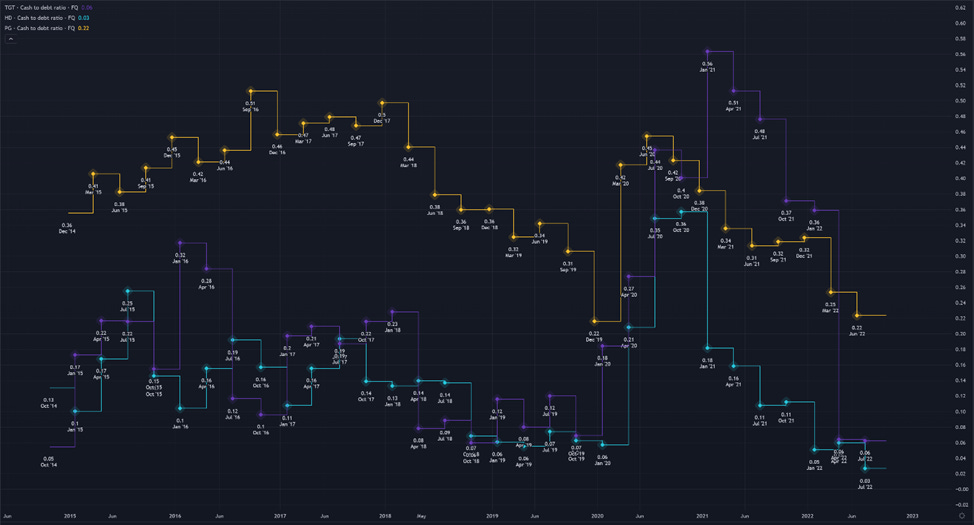

Even blue-chip companies like Target, Home Depot, and Procter & Gamble have been adding to their huge piles of debt while their cash position winds down.

Here, you can see the cash/debt ratios for Target (purple line), Home Depot (green line) and Procter & Gamble (yellow line):

Source: TradingView

These are all well below 1, which means these companies have more debt than they do cash. That’s not a problem in and of itself, but considering the potential for a liquidity crisis — as well as the fact that debt is more expensive and harder to come by — you don’t want to see these lines trending downward.

There are dozens of huge companies like these that are in serious trouble because of their reliance on debt. And I think that as we go through the next three or four earnings seasons, this will become very apparent to the market.

Of course, this is assuming that rates will stay relatively high for some time and the Fed won’t give away bailout money.

The way I see it, the ability to be self-reliant as a business right now is more important than it’s been in a very long time. That means that a business should be able to fund itself with its current cash position, in addition to future cash flows.

It’s actually a little funny that this isn’t seen as normal!

That’s why the stocks I focus on generate enough cash flow to sustain their business, don’t rely on debt, don’t waste money on share buybacks or dividends (or even worse: borrow to do that), and have products that the world wants more of.

These are the investments that will be increasingly in-demand as we move forward. With each share repurchase halt, dividend cut, negative earnings surprise, debt default, or whatever other liquidity issue we see … it’ll become that much clearer which stocks to hold.

That’s all I have for today. Make sure to check out my next Substack on Friday!

Excellent commentary Ian! Thank you.

Another great macro view, Ian...thanks!